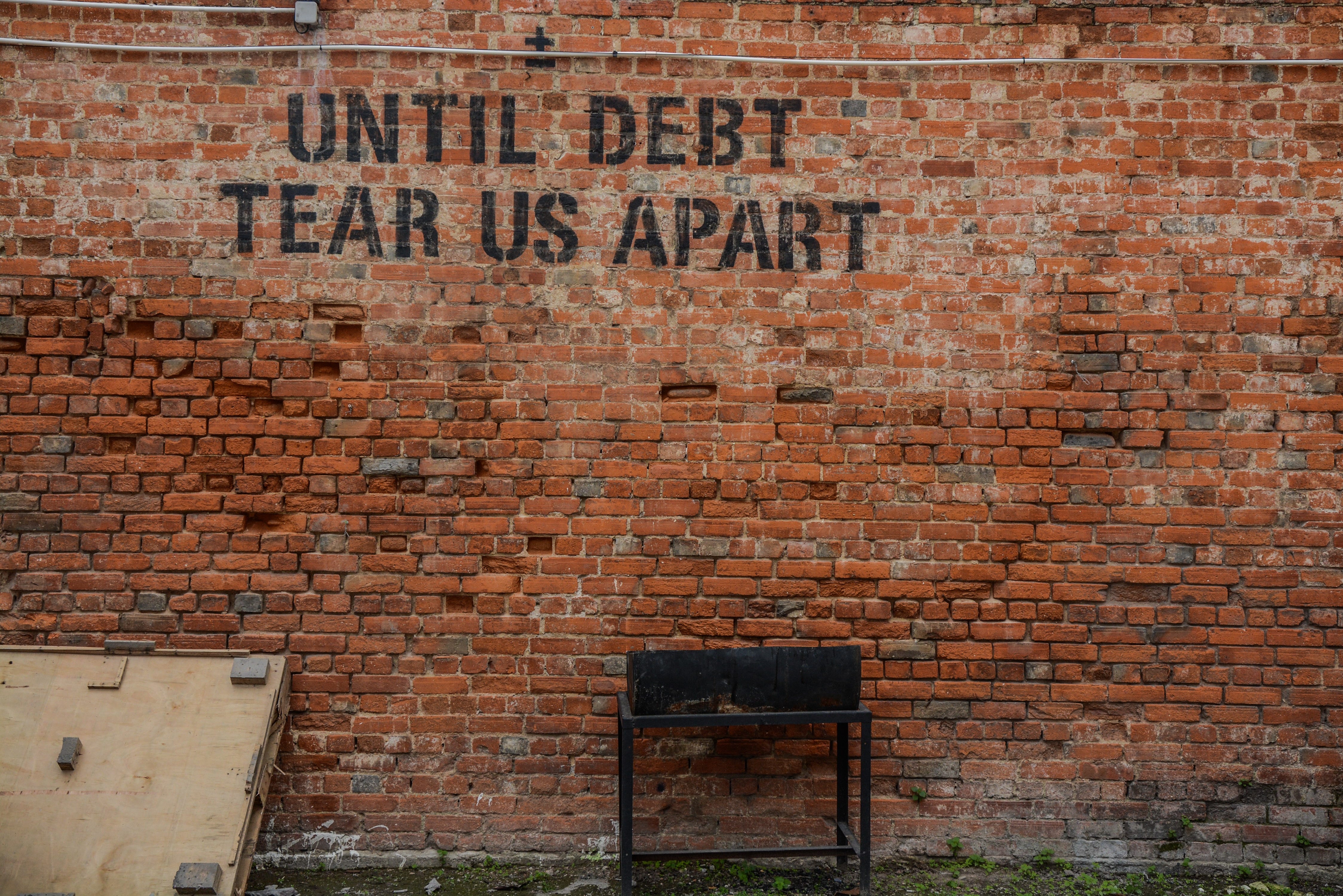

We are in debt - for life

Watching numbers ruin our lives and getting tangled in the erosion of sanity.

When I was 25 and standing in the lobby of the office building I was working in, a young girl, even younger than me, approached and almost begged me to register for a credit card. "Please, just register it; the first-year fee is free. If you don't use it, throw it away, and you don't lose anything. Please help me to get enough customers this month. Please."

Back then I didn't know what a credit card was and how it was different from a debit card or a domestic atm card. It didn't matter. I wouldn't use it. I just helped out an employee struggling to make ends meet. But, of course, I did use it. And get into debt.

But my salary was good, and I was OK to pay it off every month. Until I suffered from working-related depression, and things went out of hand. I shopped almost every week for things I couldn't use.I wandered in malls and purchased things irrationally. Once, I bought a Charles & Keith dress for $300. It left a bitter taste in my mouth when I cleaned up my place and saw the leather peel off, although I only wore it twice. When I moved back home, I threw away a big bundle of those ridiculous expensive products. Another problem, I got overweight and had drinking issues, so most of the clothes I bought couldn't fit after two or three weeks. I worked hard but barely made enough to cover the credit card debt. I had to pay a lot of fine fees for late payments. I got deeper into this fear of being unable to pay off the credit card, and the debt collectors would come to me.

Luckily that didn't happen. My close friend took me into her care and asked me to exercise and stop drinking. When I lost my first two kilos and was sober for a month, I suddenly thought of the credit card and printed out all the statements in the most recent two years. Over the last 18 months of depression, being overweight, suffering neck pain, back pain, and heavy drinking, I managed to stack up the fine fees over seven times more than my real debt. Basically, I just paid the fine, and not any debt in that card. Only after I was sober did I observe what went wrong in my habit.

I recently read the book Poverty, by America by Matthew Desmond. This author described how poor people get into deeper poverty through financial services. Here is a paragraph from the book describing online financial services and buy-now-pay-later scheme, targeting younger, tech-savvy clientele:

"You take out a small loan, usually for less than $500, and are typically charged a percentage or fee per $100 borrowed. A charge of $15 per $100 lent might sound reasonable, but it equates to an annual percentage rate of 400 percent. The loan officer requires a way to claim payment when time is up—access to a bank account or a postdated check for the full amount of the loan plus fees. Most loans are for two to four weeks, until the next payday, hence their name.

Except that when the loan comes due, you usually still happen to be broke. So you ask for an extension, which will cost you. If you took out a two-week $400 loan with a $60 fee ($15 per $100), the loan officer might allow an extension if you pay the $60 fee when the original loan comes due. Then he will issue another fee, say for an additional $60. Just like that, you are charged $120 for borrowing $400, and that's if you ask for only a single extension."

I was not surprised to see the scenario that the author mentioned as you have to pay $120 for borrowing $400 because I was there, did that, and deeply understood being financially illiterate cost me so much. I stopped at the late spot. I wish I had done things differently when I was 25 and said no to the credit card sales girls in the lobby that day. But yeah, what those companies target is us, young and clueless, desperate for a job, desperate for some slack of spending, desperate to buy something for whatever reason at the moment.

Recently, I joined a Facebook Group of people who want to commit suicide (yeah, there are groups like that). 50 percent of the posts I read every day are from people getting into debt and can't get out. "I owed the loan sharks 250 million VND (about $12,000). They threatened to kill me. Should I kill myself first?" One post wrote.

"I was trapped playing a financial app online to get high-interest rates, now I owe my relatives 400 million VND (about $20,000). I am such a bad husband, father, and son. I will lose my face if my parents and my wife find out. I just want to end it all," another anonymous person posted.

Nobody knew how many people got trapped in those money-earning apps, or cut-throat interest-rate financial services, but we read news about people jumping off their apartments because of debt quite often. Miraculously, rarely do any public media write detailed guides to inform young people about how they risk getting into debt and the hands of loan sharks.

Polished websites under attractive names, such as "high-interest game", "high-interest opportunity for your cash", "easy loan", "one-minute loan", and "Smooth loan, no paper needed," run aggressively on keyword searches about loans, or borrow money. Just one click, some steps. Done. You get your easy loan. Or now you can start earning high-interest rates for your miracle savings.

One time, I was at my mom's when my cousin arrived. He often visited my mom, persuading her to join his "financial network" by committing $250 first. My mom never believed in easy money, partially because she grew up during the stock rush and witnessed her older brother and younger brother losing all their money in a fake company. She said no. The cousin turned to persuade me. He opened the app, which looks like a Bitcoin platform but in Vietnamese. He said he earned 10% every week.

"Where do you think the money comes from?" I asked.

"The algorithm runs," he answered.

"What algorithm?"

"Here, you see it."

"They are created by people. Who are you talking about?"

"I don't know. People do not run it. It runs on it own."

"Who gives you the interest rate? Should I just type the number?" I cornered him.

Some months later, Mom called to tell me he lost all his savings from three years working as a teacher in that app. He couldn't take his money out.

My cousin is a teacher. People think that educated people might know what they are doing, but when it comes to greed, everyone is as illiterate as each other.

There are thousands of apps created to trap small amounts of cash from poor people, students, and young workers, and to trap large amounts from wealthy people who are greedy and careless enough to try new ways of getting rich. The other day I joined a group and counted the number of apps to borrow and to loan money, to bet and to "invest" that are marked as "unable to pay out", or "you can't withdraw your money". There are 13 of them in my three-minute joining group. They are updated by victims who lost money in this digital wildland.

Those are "illegal" online apps you found online. You suffer for your lack of wise judgment or you just "heard" about crypto or NFT somewhere, and those apps might be those opportunities you need to snatch right now. In a hurry, you made bad decisions without doing research. You are the victim of the tech-savvy scams.

How about legal and legitimate financial services you find in the city, at your office buildings, in the shopping malls or at phone shops, you name it.

I wondered why so many young professionals can afford to change the new iPhone and Samsung Note every so often, not like some developed markets like the US or Singapore, where you can change your old phone for the new one at a discount rate. In Vietnam, most young people pay full when new phones are on the shelf.

Then I realized the phone companies could guide you to use the scheme buy-now-pay-later or 12-24 months installment. The process is simple and smooth. You get your phone after 30 minutes of approval. You pay monthly at a reasonable rate compared to your salary. By simple calculation, you can see that you are paying the price of 1,5-2 phones for one phone. And your phone loses its value after a year. If you miss some installment, it can accumulate up to three phones when you finish the payment.

"But I will earn much more with this phone. It will bring better wealth for me," that is the most common excuse whenever I ask why they make such an irrational decision with money. I doubt an office worker would be judged because she uses a cheaper phone. Could a factory worker be judged by using a regular Android phone? Or could those phones buy them better positions in their careers?

If my clients had ever judged my work by looking at my phone, they might have judged me very hard because I have been using a $40 phone for three years with all the chipped marks on its screen. Or I may be unable to feel wealth coming to me because I don't want to pay for that.

How about if you not only buy a phone but you also buy a motorbike, a fridge, a luxurious stove, a high-end kitchen top? The products all accumulate the interest rate and installments similarly, either from the financial services or your credit card companies. Some people made a rough calculation and found out that if they took the money from the credit card to "invest" on those digital platforms, they could get better interest and earn money without working. Then we saw so many people lose their sleep over debt or moaning about their lost money.

If I could choose to live again in my 20s, I might just download some simple books to learn to calculate credit debts and installments to see how it impacts my mental health and social life. In just two paragraphs in the book Poverty, by America, Matthew Desmond illustrates how a person gets tangled up in the scheme of debt and fees, constantly being ripped off, and can't get better no matter how much they work.

Getting a new phone, dress, bike, and stove is cool, but working to death to pay for the momentary coolness is the last thing I want to exchange. Honestly, miserable people like me didn't even get that coolness. I spent my 20s buying stupid things piling up my depression until I decided to throw them into the garbage bin and reclaim my life back. They were all ugly low-quality stuff when I threw them away. It took me two freelancing years to pay off my credit card debt. I should have kept that pile of ugly clothes to remind me how materialistic I became from depression and financial crisis. I closed my credit account and never used it again.

Some friends asked me to keep a credit card "just in case" for my traveling. I keep some small cash here and there. I have some debit cards that have reasonable yearly fees and don't often change their fees too much. It doesn't look cool not to swipe or tab or spend lavishly for weekend dinners. But I get to live light, to live a life that doesn't breathe debt. I don't need that "just in case" I would overspend and get my life out of control again.

Photo by Alice Pasqual on Unsplash